Hsmb Advisory Llc for Beginners

Hsmb Advisory Llc for Beginners

Blog Article

How Hsmb Advisory Llc can Save You Time, Stress, and Money.

Table of Contents5 Simple Techniques For Hsmb Advisory LlcFacts About Hsmb Advisory Llc RevealedTop Guidelines Of Hsmb Advisory LlcThe Only Guide for Hsmb Advisory LlcThe Single Strategy To Use For Hsmb Advisory Llc

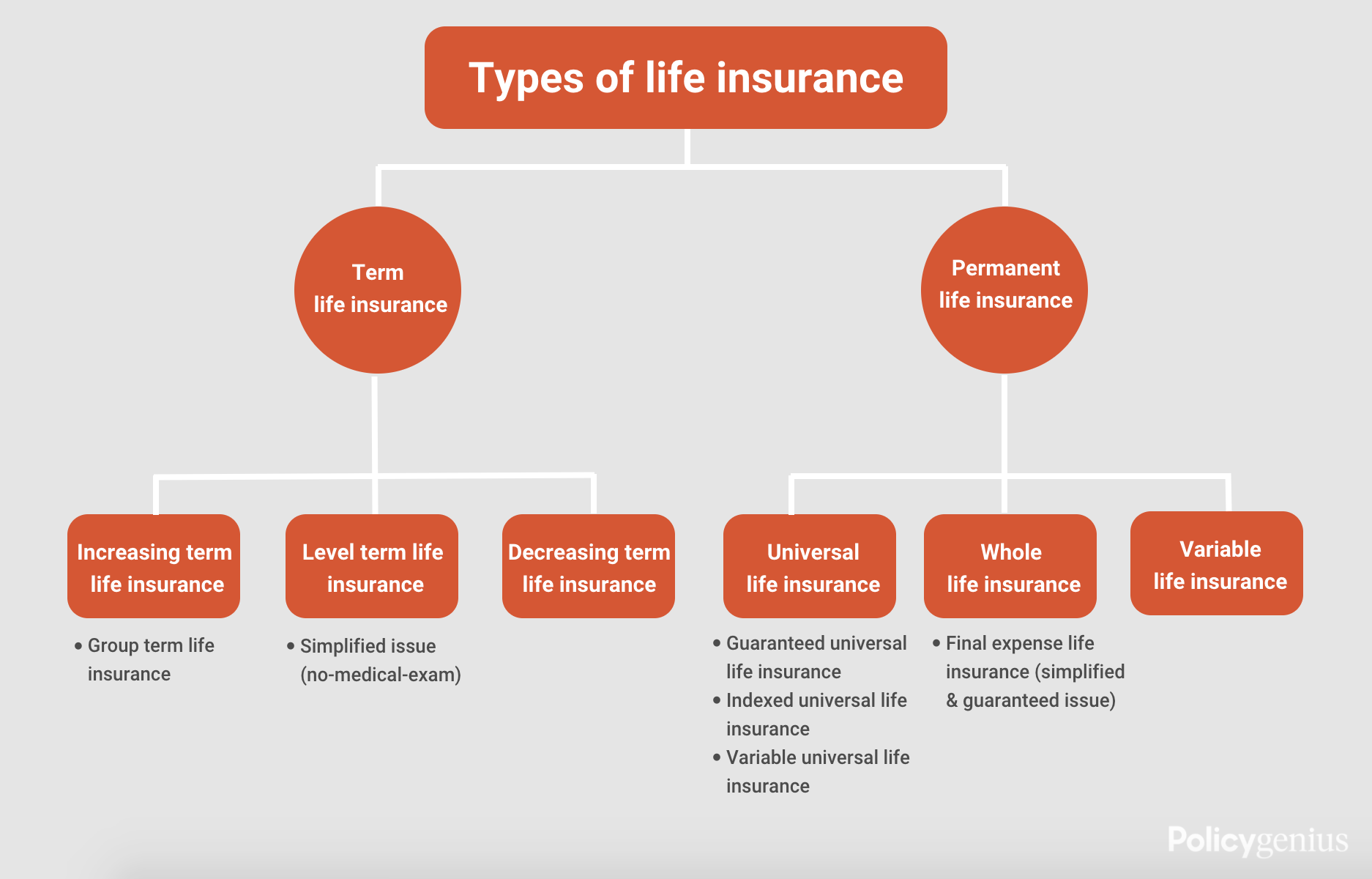

A variation, called indexed universal life insurance coverage, gives a policyholder the option to separate money value amounts to a repaired account (low-risk investments that will certainly not be impacted by the stock market) or an equity indexed account, such as Nasdaq 100 or the S & P 500. https://www.anyflip.com/homepage/gbgra. The policyholder has the choice of just how much to assign to every accountThese plans are called joint or survivorship life insurance policy and can be either first-to-die or second-to-die policies. A first-to-die joint life insurance coverage plan implies that the life insurance coverage is paid out after the first individual dies.

These are normally used in estate planning so there is enough cash to pay estate taxes and various other costs after the fatality of both spouses. For instance, let's claim John and Mary secured a joint second-to-die policy. So one of them is dead, the plan is still active and doesn't pay out.

Some Of Hsmb Advisory Llc

This ensures your loan provider is paid the equilibrium of your home loan if you die. Dependent life insurance policy is coverage that is supplied if a spouse or reliant youngster dies. This sort of insurance coverage is normally utilized to off-set expenditures that happen after death, so the quantity is normally little.

The Greatest Guide To Hsmb Advisory Llc

This kind of insurance coverage is additionally called burial insurance. While it might appear odd to take out life insurance policy for this type of activity, funeralseven easy onescan have a price tag of a number of thousand dollars by the time all prices are factored in.

We're right here to help you damage via the mess and discover even more concerning one of the most popular type of life insurance policy, so you can decide what's ideal for you.

This page gives a glossary of insurance policy terms and definitions that are commonly made use of in the insurance service. New terms will be included in the glossary with time. The meanings in this reference are established by the NAIC Study and Actuarial Division personnel based upon numerous insurance coverage referrals. These definitions stand for an usual or general usage of the term.

Unknown Facts About Hsmb Advisory Llc

- unforeseen injury to an individual. - an insurance contract that pays a mentioned advantage in case of fatality and/or dismemberment brought on by crash or defined sort of accidents. - period of time insured have to sustain eligible clinical costs at least equivalent to the insurance deductible quantity in order to establish a benefit period under a major clinical cost or extensive clinical cost policy.

- insurance provider properties which can be valued and included on the equilibrium sheet to determine financial viability of the company. - an insurance coverage firm certified to do company in a state(s), domiciled in an alternate state or nation. - happen when a policy has actually been processed, and the premium has actually been paid prior to the efficient day.

- the social sensation whereby individuals with a greater than typical likelihood of loss seek greater insurance policy coverage than those with much less threat. - a group sustained by participant firms whose feature is to collect loss stats and release trended loss expenses. - an individual or entity that directly, or indirectly, with one or even more various other individuals or entities, controls, is controlled by or is under typical control with the insurance firm.

Getting The Hsmb Advisory Llc To Work

- the maximum buck quantity or total quantity of insurance coverage payable for a solitary loss, or several losses, during a policy period, or on a solitary project. - method of reimbursement of a health insurance with a corporate entity that straight gives treatment, where (1) the wellness strategy is contractually needed to pay the total operating expense of the business entity, much less any earnings to the entity from various other users of services, and (2) there are mutual limitless assurances of solvency in between the entity and the health insurance that put their respective capital and excess at threat in guaranteeing each other.

- an insurance coverage firm created according to the regulations of an international nation. The firm should conform to state regulatory criteria to legally market insurance policy items in that state. - insurance coverages which are generally written with home insurance, e.- an annual report required to be filed with each state in which an insurer does business.

Report this page